skip to main |

skip to sidebar

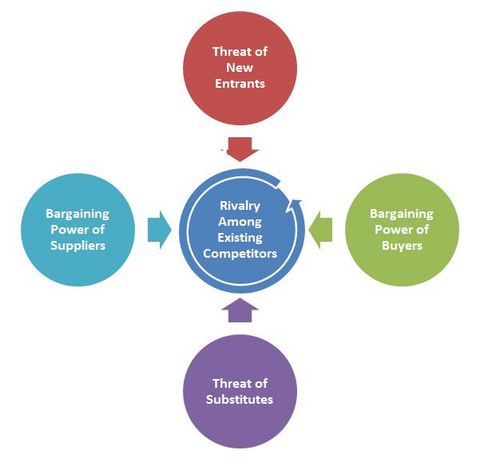

Porter's 5 forces analysis - Global Telecom Industry

Threat of New Entrants. It comes as no surprise that in the capital-intensive telecom industry the biggest barrier to entry is access to finance. To cover high fixed costs, serious contenders typically require a lot of cash. When capital markets are generous, the threat of competitive entrants escalates. When financing opportunities are less readily available, the pace of entry slows. Meanwhile, ownership of a telecom license can represent a huge barrier to entry. In the U.S., for instance, fledgling telecom operators must still apply to the Federal Communications Commission (FCC) to receive regulatory approval and licensing. There is also a finite amount of "good" radio spectrum that lends itself to mobile voice and data applications. In addition, it is important to remember that solid operating skills and management experience is fairly scarce, making entry even more difficult.Power of Suppliers. At first glance, it might look like telecom equipment suppliers have considerable bargaining power over telecom operators. Indeed, without high-tech broadband switching equipment, fiber-optic cables, mobile handsets and billing software, telecom operators would not be able to do the job of transmitting voice and data from place to place. But there are actually a number of large equipment makers around. There are enough vendors, arguably, to dilute bargaining power. The limited pool of talented managers and engineers, especially those well versed in the latest technologies, places companies in a weak position in terms of hiring and salaries.

Power of Buyers. With increased choice of telecom products and services, the bargaining power of buyers is rising. Let's face it; telephone and data services do not vary much, regardless of which companies are selling them. For the most part, basic services are treated as a commodity. This translates into customers seeking low prices from companies that offer reliable service. At the same time, buyer power can vary somewhat between market segments. While switching costs are relatively low for residential telecom customers, they can get higher for larger business customers, especially those that rely more on customized products and services.

Availability of Substitutes. Products and services from non-traditional telecom industries pose serious substitution threats. Cable TV and satellite operators now compete for buyers. The cable guys, with their own direct lines into homes, offer broadband internet services, and satellite links can substitute for high-speed business networking needs. Railways and energy utility companies are laying miles of high-capacity telecom network alongside their own track and pipeline assets. Just as worrying for telecom operators is the internet: it is becoming a viable vehicle for cut-rate voice calls. Delivered by ISPs - not telecom operators - "internet telephony" could take a big bite out of telecom companies' core voice revenues.

Competitive Rivalry. Competition is "cut throat". The wave of industry deregulation together with the receptive capital markets of the late 1990s paved the way for a rush of new entrants. New technology is prompting a raft of substitute services. Nearly everybody already pays for phone services, so all competitors now must lure customers with lower prices and more exciting services. This tends to drive industry profitability down. In addition to low profits, the telecom industry suffers from high exit barriers, mainly due to its specialized equipment. Networks and billing systems cannot really be used for much else, and their swift obsolescence makes liquidation pretty difficult